Analysis comparing wage, revenue and inflation over the past two years shows the coffee industry is paying its staff more by raising prices

Listen to this article and subscribe to get future audio articles

In 2017 United Baristas wrote a series of articles on coffee shop profitability and staff wages. We were concerned that the industry was charging consumers too little, and a culture of hyper-competitive benchmarking meant coffee shops were seeking to be simultaneously faster, cheaper and better than their competitors – rather than allowing their shop’s proposition to develop into viable niches.

Some previous articles

• Insights from the Iron Triangle

• How Baristas Can Get Paid More

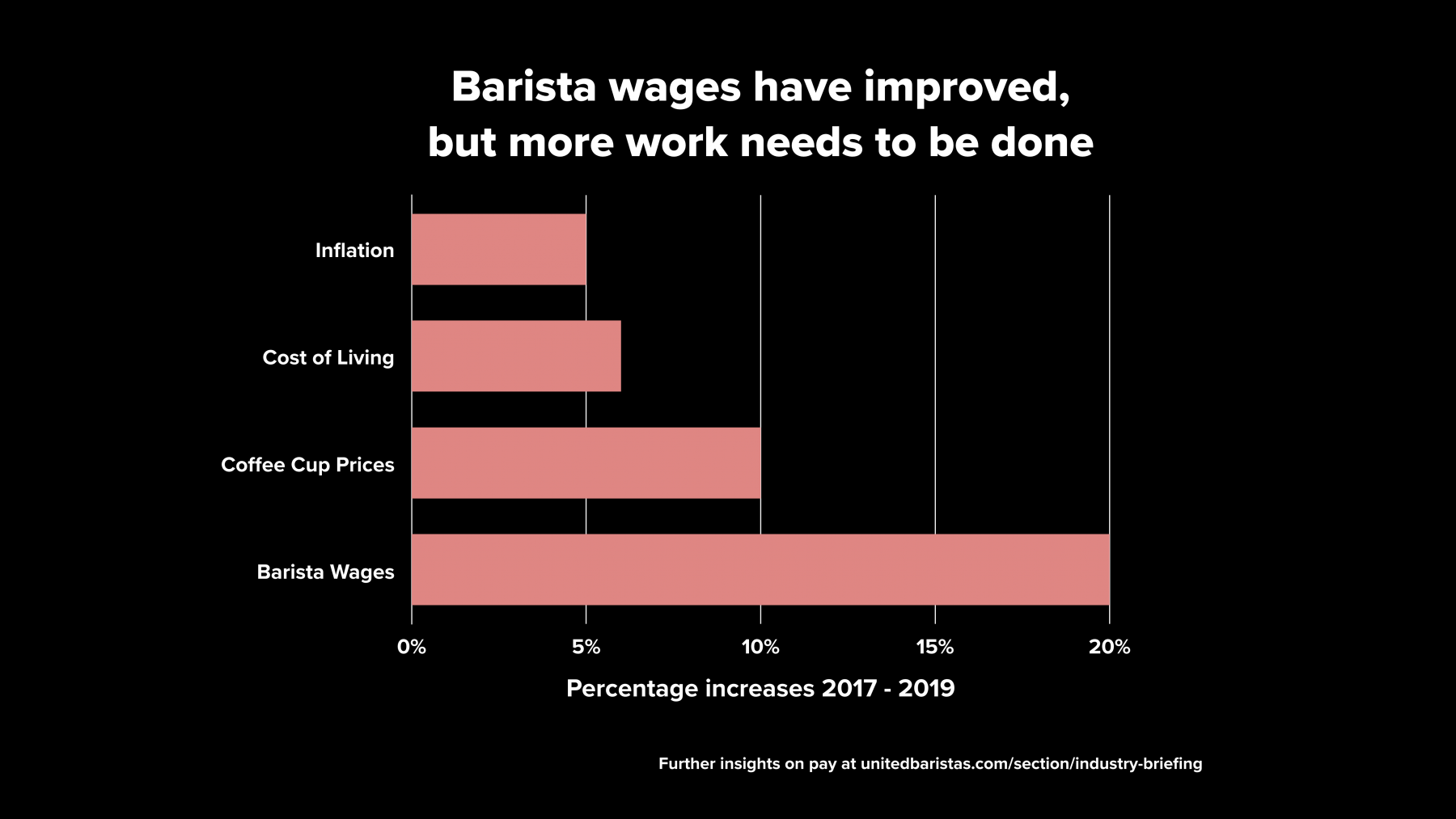

Industry and economic data indicates the industry is making progress on a number of fronts. Increases in cup prices have outstripped general inflation as well as the Consumer Price Inflation (CPI) – and much of that price increase is going towards shop staff wages.

| Change 2017 – 2019 | |

|---|---|

| Inflation | up ~5% |

| Consumer Price Inflation | up ~6% |

| Cup prices | up ~10% |

| Barista wages | up ~20% |

At a headline level, this means an average shop’s revenues should be up more than its costs, and assuming staff costs running at 30% of revenue, a significant proportion of that revenue is being directly passed on to staff. While some of the increased revenue will be lost to increased expenses, much of the balance is presumably being adding to the bottom line.

In the second half of 2017 a significant number of baristas were working for the legal minimum wage (which is called the National Living wage) of £7.50 per hour. Today it is more commonplace for baristas to be working above the current National Living wage of £8.21, and also the forthcoming rate of £8.72 from 1 April 2020. An increasing number of coffee companies are paying the Living Wage Foundation rate of £9.30 for the UK, or £10.75 for London.

Overall these developments are welcome. The coffee industry operates in a broader competitive environment and needs to offer levels of pay that are sufficiently high enough to both attract and retain talent from other industries.

Increased coffee shop profitability is also to be welcomed. As raised in 2017, many shops were operating on razor-thin margins, and we have since seen a number of coffee shop companies pass into administration or become defunct. Entrepreneurs, owners and investors need to make a sufficient return on capital and their time to justify their investment and the risks that they carry. Improved profitability helps to ensure the ongoing prospects for the industry.

Behind the headlines

A more detailed look is maybe more concerning on both wage costs and profitability fronts, and the medium-term outlook remains uncertain.

Staff costs

United Baristas has been advocating for price rises to lift profitability and to pay staff more. In reality while this has come to pass, the driver of wage increases has been a reduction in the number of young Europeans coming to live in the UK following the Brexit referendum. With a smaller pool of talent, wage costs have increased, and those costs have been passed on to consumers in the form of price increases.

Today it is highly uncertain as to what future arrangements will be negotiated between the UK government and the EU for when the transition period ends in 2021. As a consequence, we expect staff wages to rise again over 2020.

Companies are also now legally obliged to make pension contributions, which are not reflected in the above headline figures.

Coffee Shop Profitability

It is harder to examine the industry’s profitability, but it is widely appreciated that the range of profitability extends from the loss-making to the financially lucrative.

This is typical of most industries and it is hoped that the better operators are able to create more profitable businesses; although there is some evidence to suggest that this hasn’t always been the case of the past two years.

As we noted then, low barriers to entry and a hyper-local market catchment make coffee shops particularly vulnerable to new market participants who open a store, naively undercut on price, run at a loss in an attempt to seize market share, and in doing so reduce or eliminate the profitability of the incumbent and themselves – all too often with terminal consequences.

This is the nature of business, and not unique to coffee shops. But coffee shops are maybe uniquely vulnerable because of the relatively high capital investment in site infrastructure making relocation financially difficult for many small and medium coffee shop businesses, compared to say a florist or retail store.

Looking forward

The present trends are likely to continue because the drivers of those trends remain largely unchanged.

Coffee shops need to be thinking deeply about how they will structure their operations and proposition in order to be able to pay higher rates of pay, and provide the right level of profitability to justify their investment.

There are increasing signs that the specialty coffee market is finally segmenting into niches. For example, a number of brands are now sourcing cheaper green while others are regularly spending circa twice and working to build premium brands with premium pricing.

It is now also reasonable to wonder if, after a decade of rapid growth, specialty coffee has saturating its natural market niche, as total shop numbers grow only a little in the main urban UK cities. Beneath the more static headline numbers there is significant market churn. Each month as many as a dozen shops open, and others close, in London.

United Baristas welcomes a maturing market which seems to be naturally settling around a market volume, retail prices, cost structure, and return on investment. Increased normalisation and clarity of these figures, such as in the more mature coffee markets in the United States and Australasia, is to be both welcomed and expected.

Other trends

If you have experience or insights on the factors shaping coffee shop profitability, please comment below or get in touch via the usual channels

References & data

- Inflation & Consumer Price Inflation (CPI): Office for National Statistics

- Cup prices: anecdotal evidence, assuming shift from circa £2.70 in Q4 2017 to £3.00 in Q4 2019

- Barista wages: job listings United Baristas Jobs and UK Government

Give Coffee If you found this article useful, show your appreciation

Give Coffee If you found this article useful, show your appreciation